By

By

By Niall McCracken

FIGURES obtained by The Detail reveal that nearly three times as many property owners in Northern Ireland faced repossession through the courts than those in the Republic of Ireland between 2008 and 2011.

While the public focus in recent years has been of the pain suffered in the Republic of Ireland (ROI) because of the high profile of its property crash, we have spoken to leading economic and housing experts who say the experience in the North has been far more severe.

The data obtained and analysed by The Detail reflects only the experience of repossessions processed through courts and is not the full picture of mortgage “distress” in both jurisdictions. But it does show profound differences in policy on both sides of the border: how banks in the south have been inclined to allow many mortgage cases to languish “unresolved” within the Irish justice system; and how the courts then deal with mortgage cases.

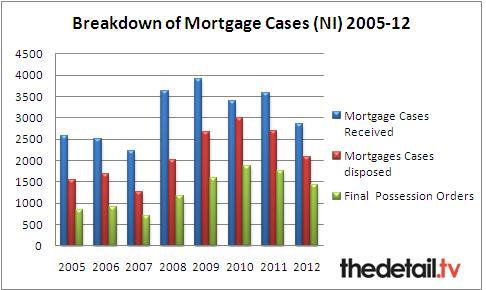

Figures obtained by The Detail in response to a Freedom of Information request submitted to the Northern Ireland Court Service show that over 10,000 property owners in Northern Ireland were ordered by a court to deliver possession of their property over the last eight years. Of these cases, 3,000 resulted in forced evictions following a failure to abide by the original court judgment.

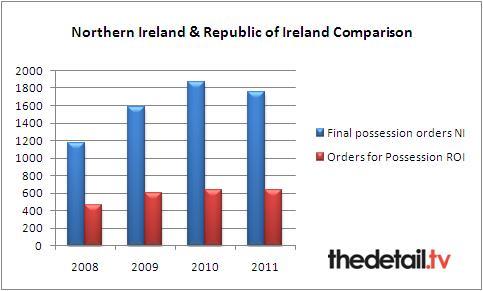

Since the 2008 crash and 2011 there were 6,337 Final Possession Orders in Northern Ireland. Over the same period in the Irish Republic there were 2,327 Orders for Possession granted in the High Court and the Circuit Courts in the Republic of Ireland.

These figures show three times as many repossessions being ordered by the courts in the North than in the South, but when the size of the two jurisdictions’ populations are taken into account – the Irish Republic’s being two-and-a-half times bigger than the North’s – the rate of repossessions through courts in the North is proportionately almost seven times that of the Republic.

The figures on both sides of the border reflect repossessions of all types of property. However domestic properties are likely to comprise the majority; indeed the development of a pre-action protocol in the courts in the north reflects a preoccupation with residential property rather than any other type.

Housing expert Paddy Gray, from the University of Ulster, said that the differences between the two jurisdictions was “stark” and that the high rate of repossession in Northern Ireland would have a knock-on effect on homelessness and demand for social housing. He urged Northern Ireland’s politicians to address the issue before it reached crisis point.]

Today we also map possession orders throughout Northern Ireland, click here to read this story.

ORDERING A REPOSSESSIONThe figures we are reporting on today concentrate on Final Possession Orders, or Orders of Possession as they are known in ROI.

In Northern Ireland a Final Possession Order (FPO) occurs when the court makes a ruling to deliver possession of the property within a specified time. A homeowner will only avoid repossession if an agreement can be reached with the bank/building society on repayments.

Figures for 2012 only for January to September (NI court service)

There are a number of avenues available for mortgage cases within the Northern Ireland court system:

- Any potential repossession will start with a mortgage case being submitted to the NI court service. A mortgage case is when a writ or originating summons has been issued in respect of default on the repayment of a mortgage. The case is then considered as “disposed with” when a final order, such as a Possession Order is issued.

- A case disposed may not always be a final order for repossession. Other orders include Final Suspended Possession Orders. In this case the court may postpone the date for delivery of possession if it is satisfied that the defendant is likely, within a reasonable period, to pay any sums due under the mortgage, or to remedy any other breach of the obligations under the mortgage.

- Other orders can also include strike out or dismissal action. This occurs when the moving party does not wish to proceed any further, or when the court rules that there is no reasonable ground for bringing or defending the mortgage.

- When there is a failure to deliver possession of a property following a final possession order, the Enforcement of Judgments Office (EJO) has statutory power to enforce the order. Click here for more detail on EJO figures.

The figures show that 2010 featured the highest number of Final Possession Orders with almost 1,900 cases in Northern Ireland alone. The number of Possession Orders granted over the last seven years has more than doubled in Northern Ireland with a total of 837 in 2005 and 1,753 in 2011. For a full geographical breakdown of the number of possession orders across Northern Ireland since 2005 click here.

The Lord Chief Justice’s Office in Northern Ireland announced on 30 August 2011 that the ’Pre-Action Protocol for Possession Proceedings based on Mortgage Arrears in respect of Residential Property’ had been revised. The basic premise of the original protocol was to reduce repossession court proceedings through negotiation and exploring alternative ways of reaching a settlement.

The revised protocol set out the steps that lenders are expected to take before bringing a claim in the courts. It states that lenders should ensure that repossession action is a last resort and that lenders are expected to demonstrate that they have tried to discuss and agree alternatives to repossession with borrowers when they encounter difficulty with their mortgage repayments. The Protocol states:

“It is in the interests of the parties that mortgage payments or payments under home purchase plans are made promptly and that difficulties are resolved wherever possible without court proceedings. However in some cases an order for possession may be in the interest of both the lender and the borrower.”

For access to the full document click here.

The most up-to-date figures released to The Detail by the Northern Ireland Court Service outline that from January to September 2012 there were a further 2,855 mortgage cases received: 2,000 were disposed and 1,400 of these were possession orders.

For a full breakdown click on the Excel sheet below this article.

A spokesperson for the Department of Social Development said: “In August 2011, Minister [Nelson] McCausland announced over £500,000 funding for the Mortgage Debt Advice Service that will ensure the continuation of the advice service delivered by Housing Rights Service, until March 2015. Minister McCausland has also secured additional funding in the current financial year to help the service deal with the increased demand for assistance from those facing mortgage difficulties.

“This DSD-funded service operates during office hours and also provides alternative forms of access, such as the online virtual advisor, as well as extended contact hours to 8pm on Tuesdays and Thursdays providing greater flexibility for those facing mortgage difficulties to take advantage of the advice services on offer. Repossession should always be a last resort.”

ACROSS THE BORDER

Data provided by Northern Ireland Court Service & Court Service of Ireland

Figures in the Irish Republic show that from 2008-2011 there were 2,327 Orders for Possession granted in the High Court and the Circuit Courts in the Republic of Ireland compared with 6,337 Final Possession Orders in Northern Ireland during the same period. Click on the Excel sheet below this article for a further breakdown.

The Republic of Ireland’s population is two-and-a-half times the size of Northern Ireland’s – so if the figures for Northern Ireland are extrapolated according to population size, the number of Final Possession Orders is 6.8 times the number in the Republic.

Similar to possession orders in Northern Ireland, orders for possession do not necessarily equate with actual possessions. However, in the Republic of Ireland It is up to the person or company who obtained the order to pursue its execution.

A spokesperson for the Court Service of Ireland said that the data collected in respect of possession orders in the Republic of Ireland may not reflect the full picture on persons losing their property as “most mortgage contracts permit the lender to foreclose for non-payment of instalment without a court order.”

The number of Orders of Possession in ROI have been significantly less

However, Goodbody Stockbrokers economist Juliet Tennent believes the figures do provide an insight into the attitude of the Irish banking system throughout the housing crisis.

She said: “The predominant policy that the banks have been following throughout the recession has been one of forbearance. What you’re seeing with these figures are the banks in the Republic of Ireland implementing a number of policies that don’t actually progress or resolve a case that is in arrears.

“One of the reasons for this could be that many of the banks have perhaps thought that the economic climate and property market would improve and they wouldn’t actually have to take action, but clearly this crisis has lasted much longer than many have expected."

Article 40 of the Constitution of Ireland holds the state to protecting “the personal rights of the citizen”, and in particular to defend “the life, person, good name, and property rights of every citizen.” Ms Tennent believes the home as an institution is embedded in the mindset of Irish society.

She said: “The idea of the ‘family home’ is certainly an emotive issue around the figures for the south of Ireland. It hasn’t been the culture to repossess this institution in the Republic and also because the legislation to do so has been very difficult in this regard. Our bankruptcy laws are archaic but there have been moves recently to bring this legislation more in line with international standards.”

Experts have pointed to a legal anomaly in the 2009 Land and Conveyancing Act that has meant that a number of repossession cases have been halted by the high court since 2011 (Dunne ruling).

Ms Tennet says the recent agreement between the Troika and the Irish Government to remove a legal impediment which has stopped banks repossessing properties, will have an a knock on affect on the number of repossessions in the Republic. Alongside this, new insolvency arrangements are also being legislated for in the Republic of Ireland.

While they are not expected to be finalised until the end of the first quarter of this year, experts say that it will offer an opportunity to tackle the mortgage problem in a more comprehensive way. Key to this will be the process of “writing off of unsustainable mortgages”.

This was a key criticism of the Central Bank in a speech given by the Director of Credit Institutions and Insurance Supervision Fiona Muldoon in October 2012.

She said: “Wait and see has become the strategy of choice. In that regard, my question four years in is what is it that we are waiting for on mortgage arrears? The hope for an economic recovery, hope that house prices will come back? This is the stuff of denial. Hope is not a strategy – any more than anger. The path to viability will be through taking each loan, each customer and working out a solution that both responds to their needs and to a bank’s need to collect where it can."

A report from Goodbody Stockbrokers from November 2012 refers to the high number of forbearance solutions implemented. It calculated that the covered banks have written down a total of just €251m of their total mortgage books over the 2010-H112 period, whereas provisions of ”€6.4bn sit on the balance sheet .”

Dermot Connolly is from the organisation Defend our Homes, based in the Republic of Ireland, which was set up to help people resist repossession. He believes the situation must be resolved as soon as possible.

He said: “Essentially I think the banks have been waiting. One of the problems with collapsing house prices is that you’re into negative equity, mortgages are at £300k and the property might only be worth £120k or £150k now. You have a situation if they go for repossession, it’s inevitable that there will be financial losses. So there definitely has been a lull.”

In 2011 the Irish Government rolled out a €24 billion recapitalisation plan for the Irish banking sector. Under the plan, the Minister for Finance Michael Noonan TD said the Government would reduce the number of domestic banks to two “pillar banks”, based around AIB and Bank of Ireland.

Mr Connolly believes this policy has been planned with the new insolvency legislation in mind. He said: "There is an argument that the recapitalisation to the tune of €24bn would act as a stress test on the property loans. The banks have been in effect given loans by the government to cushion them against write downs on bad property loans, residential and commercial. The banks are sitting on the money, but what will happen once the insolvency plans come in, is anyone’s guess.

“Certainly it seems to me that the government has pinned its hopes on this insolvency bill, this will essentially force the banks to make sustainable arrangements, in affect to write down mortgages in some cases. However, when this comes through you could see a massive amount of repossessions or people declaring themselves insolvent.”

Click here to read an analysis piece focusing on the Republic’s repossession figures written by Conor Pope from The Irish Times.

STORMONT’S ROLE

Paddy Gray says the assembly need to take a look at the rate of repossessions here

Paddy Gray is a professor of Housing at the University of Ulster and is on the board of Threshold Ireland which works with the private sector in the Republic to sustain tenancies.

He said: "The figures surprise me in one respect in that the difference of repossession rates north and south is so stark. However, through my work with Threshold Ireland, it’s clear that with the mortgage market in the south, there’s a lot more sensitivity, particularly with the government.

“Because the market had a massive collapse in the south, there are many properties lying empty. Figures say there are 3,000 ghost estates, so in a way banks don’t want to repossess and sell because they’re not going to get anywhere near the original value of the property. So they’re entering into agreements with advice agencies like us, to sustain people living in their home and working out different rates of repayments.”

Professor Gray believes the rate of prepossessions in Northern Ireland will inevitably have a knock-on effect on social housing here. There are no figures readily available to provide details of those who apply for social housing because their home was repossessed. However, in terms of homelessness in Northern Ireland, the impact of repossessions can be identified.

Figures from the Northern Ireland Neighbourhood Information Service’s (NINIS) show that Those declaring mortgage default as the reason for homelessness rose from 77 in 2004 to to 200 in 2011. Professor Gray says MLAs here have an obligation to look at this problem before it gets to crisis point.

“I think there certainly is a need for the assembly to take more recognition of this because it is going to cause more serious problems in the future. People who are repossessed will become statutory homeless and in the last year alone we’ve had 20,000 families presenting as homeless.

“That’s going to put an added burden on the social rented sector, which has been contracting in recent years whereby there’s not enough houses being built, so waiting lists will rise much further or people will continue to live in overcrowded conditions.”